Balance Transfer Credit Card Rates: 0% APR Offers to Eliminate Debt Faster

My buddy Tom was bragging last month about wiping out about $7,000 in credit card debt thanks to one of those 0% APR balance transfer offers. He felt like he’d hacked the system, and honestly, for someone buried under high-interest charges, it feels that way. You’re essentially getting a short-term financial interest-free loan; it’s a fantastic way to focus all your energy on crushing the principal amount rather than just paying the bank’s vig.

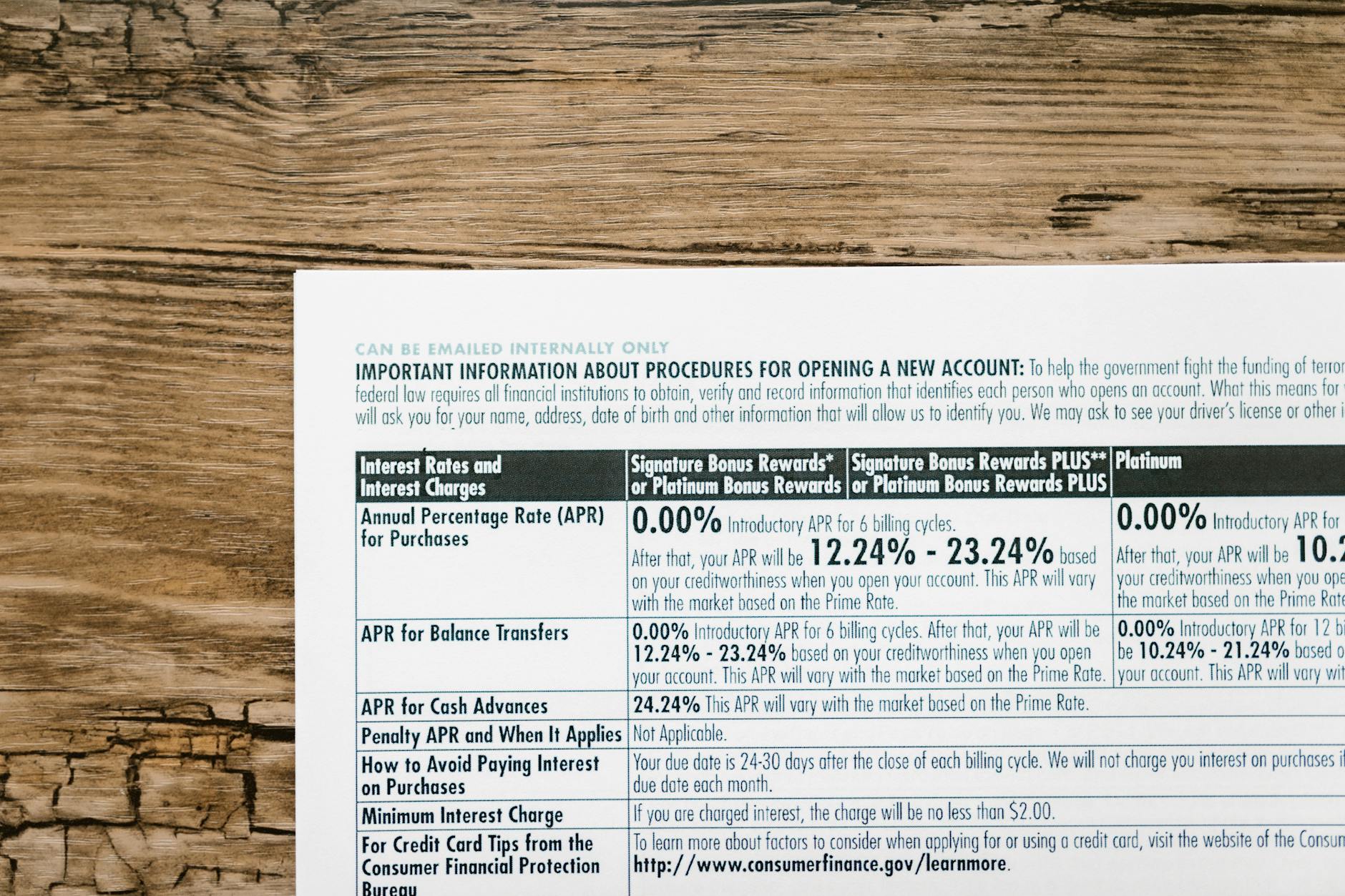

The secret sauce here isn’t the card itself, which is usually pretty boring—it’s the introductory period. You’re usually looking at 12 to 21 months where you pay zero interest on that transferred balance. If you have an existing card charging 24.99% APR, moving ten grand over means every single payment you make for that intro period goes straight toward reducing that ten grand, which is huge. I distinctly remember when I used one of these years ago to consolidate some student loan confusion—it simplified everything immensely.

A sudden three-hundred-dollar minimum payment suddenly feels manageable when you know that the entire amount is chipping away at the actual debt, not just covering the interest graveyard. The whole objective is to treat that 0% period like a ticking clock, which you absolutely must respect. Check out the Federal Reserve’s overview on consumer credit trends if you want to see how common this kind of debt maneuvering really is.

Paying off that debt within the promotional window is the whole game, though. If you mess around and still have a balance when that 0% APR period expires—say, after 18 months—you’re going to get hit hard. Most cards revert to a standard purchase APR, often around 18% to 28%, usually retroactively from the transfer date, which is a nasty surprise for those who aren’t paying close attention to the fine print. Even if it’s not retroactive, suddenly facing that high rate on whatever balance remains can undo all your hard work.

The biggest headache, the one that truly drives me insane, is the balance transfer fee. Nearly every single decent offer hits you with a 3% to 5% fee right off the bat. So, if you transfer $10,000, expect an immediate charge of $300 to $500 tacked onto that balance. You just got free interest for a year, but the bank always wants its upfront cut, and you have to build that fee into your payoff plan, or you’ve shot yourself in the foot right out of the gate. I was genuinely shocked the first time I saw that charge hit; it felt like getting nickeled and dimed before I’d even started saving money.

You shouldn’t even consider signing up for one of these balance transfer cards unless you have a rock-solid plan to pay off the entire debt within, at most, two-thirds of the promotional window. If you need 21 months, plan to be done in 14. You need buffer time for emergencies, or life simply intervenes, right? This strategy is best suited for people who have demonstrably good spending habits otherwise, meaning you aren’t just shuffling high-interest debt from one plastic card to another shiny new one. NerdWallet has some great breakdowns illustrating how the fee impacts the break-even point between different card offers.

I firmly believe that if you have significant debt floating around at 20% interest, you are actively losing money every single day, and aggressive moves like this are necessary. Don’t waste time looking at cards with introductory periods shorter than 15 months; those just aren’t worth the hassle of applying and transferring. The risk you run, beyond the fee, is that a great card like the Citi Simplicity, which has historically offered long 0% periods, might suddenly slash its offering to just 12 months because market conditions changed, leaving you with less time than anticipated.

So go ahead and chase that 0% interest, but understand you are trading a known cost (interest) for an immediate, known cost (the transfer fee), and the entire endeavor hinges on your discipline over the next year or so.