I Compared Every Online Lender: Here’s Who Actually Has the Best Rates

I spent a solid two weeks digging through the fine print of pretty much every online lender I could find. It was a rabbit hole, for sure. My goal? To figure out who’s actually offering the best interest rates on personal loans, not just the ones with the flashiest marketing.

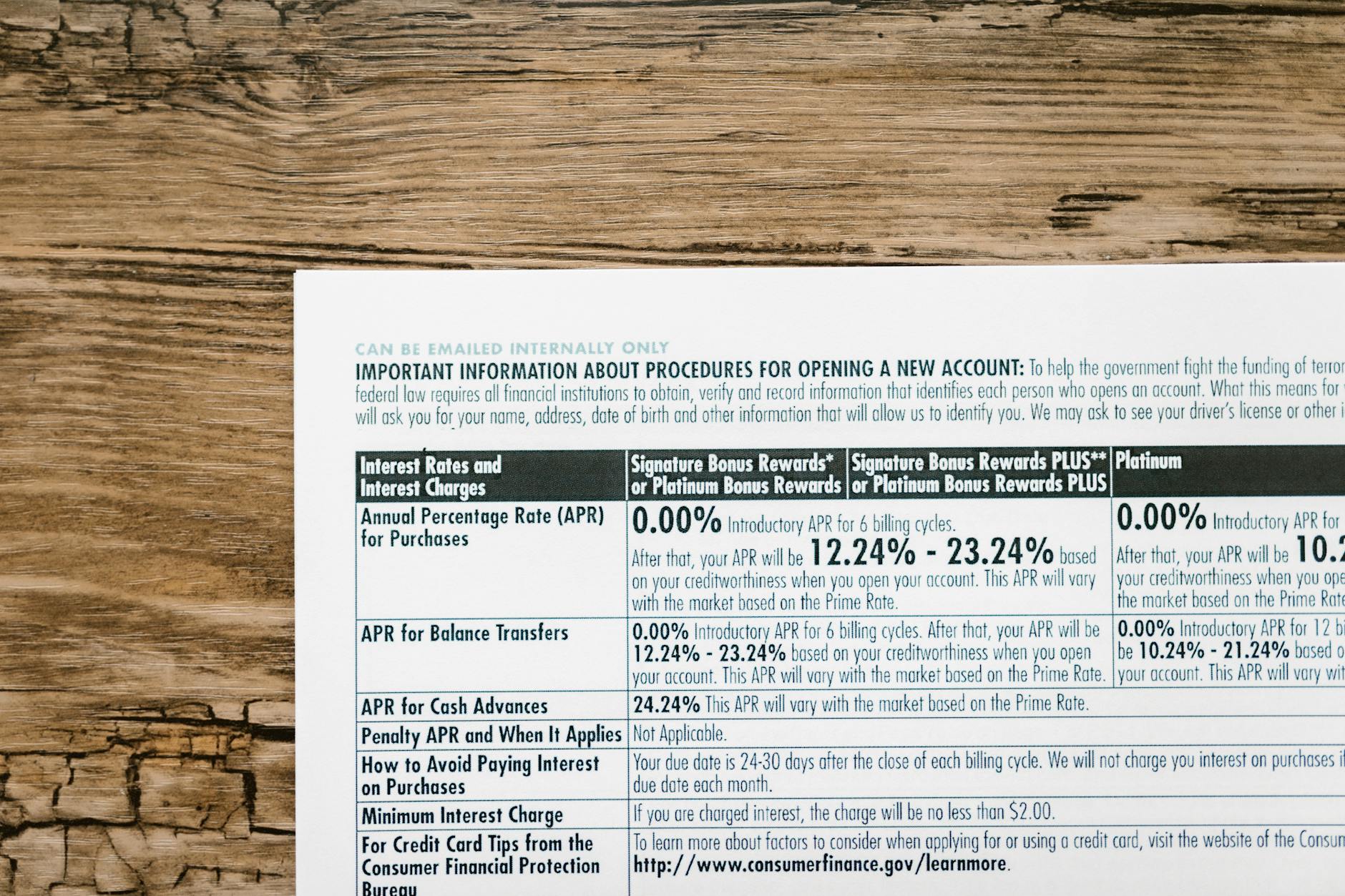

You think it’s straightforward, right? Just scan their websites, see the APRs, and pick the lowest. Ha! That’s where the frustration really kicks in. Most of them advertise a low starting rate, like 4.99%, but that’s almost impossible to get unless you have a near-perfect credit score (think 780 and up) and a super low debt-to-income ratio. It’s like they dangle it there just to get your attention, and then bam – reality hits when you get your actual offer.

So, who did stand out after all that screen time? For borrowers with excellent credit, lenders like SoFi and Discover consistently showed up with competitive advertised rates, often in the low-to-mid 6% range for those with top-tier credit. They also tend to have a pretty smooth online application process and often fund loans quickly, sometimes within a business day, which is huge if you’re in a pinch.

But here’s the real kicker, and it’s a genuine downside: the advertised rates are practically a fantasy for most people. I dug into NerdWallet’s personal loan comparison tool, which aggregates offers, and even there, the actual rates people get can be significantly higher. For someone with good, but not stellar, credit – say, a FICO score in the mid-700s – you’re more likely looking at rates anywhere from 9% to 15%, depending on the lender and loan amount. This is where LendingClub sometimes pops up, especially for those seeking slightly smaller loan amounts or who might have a blended credit profile.

I’ve got to be honest, my personal favorite for ease of use and transparency, despite not always having the absolute rock-bottom advertised rate, is Upgrade. They seem to be upfront about their fee structures and their customer service, based on the hundreds of reviews I sifted through, is generally pretty responsive. They’re not always the cheapest, mind you, but they make the whole process feel less like navigating a minefield.

The absolute biggest limitation across the board is how heavily credit score dictates everything. It’s not just about the score itself, but the length of your credit history, your payment history, and your credit utilization ratio. A single late payment from five years ago can still affect your options, and lenders like Marcus by Goldman Sachs, known for their solid reputation, are particularly stringent here. They offer competitive rates, often in the 7% to 12% range for well-qualified borrowers, but they won’t budge if your credit profile isn’t pristine.

What truly shocked me was how many lenders bury origination fees. Some, like LendingPoint, can charge up to 10% of the loan amount upfront. So, if you borrow $10,000, they could deduct $1,000 before you even see a dime, effectively raising your true borrowing cost. This is a critical point many people miss when they’re just looking at the headline APR. You need to factor in that fee when comparing offers; a slightly higher APR with no origination fee is often a better deal than a lower APR with a hefty one. You can find more on typical loan fees at Investopedia’s guide to loan origination fees.

So, to wrap this up, finding the “best” rate isn’t about finding one single lender. It’s about understanding your own financial picture and shopping around aggressively, using tools like the Consumer Financial Protection Bureau’s (CFPB) educational resources to understand what’s being offered. Don’t just look at the first offer you get. Credit unions, which operate similarly to banks but are non-profit, often have very competitive rates and are worth investigating; many local ones offer online applications now. You might find that a small, local credit union you’ve never even heard of has a better deal than the big names you see advertised everywhere.

Honestly, the entire system feels designed to make us feel worse about our financial situations, regardless of the actual numbers.