Best Rates for IRA Accounts: Growing Your Retirement Savings Tax-Efficiently

I remember back when I first opened my IRA account; I spent two full weekends just comparing the minor differences in expense ratios between Vanguard and Fidelity offerings. Seriously, it felt like I was trying to buy a car based on tread wear. We’re talking about tax-advantaged growth, right? That’s the whole payoff for keeping your money locked up for decades.

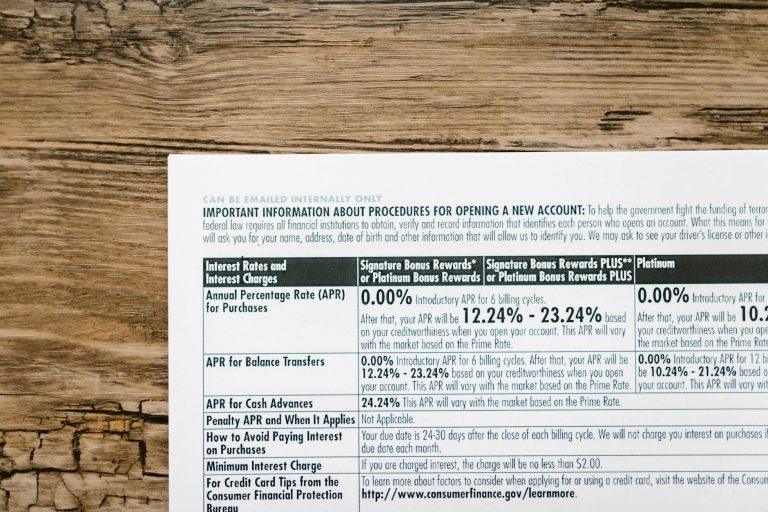

You’ll find most of the major brokerages—think Schwab, Fidelity, Vanguard being the big three—offer zero-commission trading now. That used to be a huge selling point, charging maybe $10 a trade just to buy an index fund. Today, the rate you’re chasing isn’t commission; it’s the interest rate on cash holdings or the expense ratio on any proprietary funds you might look at.

The best “rate” for a Roth IRA or a Traditional IRA generally isn’t an interest rate you earn, which is a common point of confusion for newcomers. You’re usually just holding stocks, bonds, or ETFs. The actual return rate is determined by the market, not the custodian. However, some brokerages will offer a slightly higher interest rate, maybe 4.0% or so recently, on uninvested cash balances sitting right there in the IRA wrapper, which is a small perk if you tend to keep a buffer before deploying capital. Check out what NerdWallet says about current cash sweep rates; they update it fairly often.

My personal opinion? Don’t obsess over the 0.03% difference in expense ratios between two S&P 500 trackers. If you pick a reliable, low-cost fund like VTSAX or just an equivalent total stock market ETF, you’ll be fine. The biggest mistake people make is not maxing out their contributions annually, not arguing over basis points on administrative fees.

What cracks me up is how many platforms advertise “High-Yield Savings Accounts” when they are just referring to the cash sweep inside your IRA. It’s marketing fluff. For example, if you’re retired and drawing distributions, you need to be aware of the Required Minimum Distributions (RMDs) starting around age 73 now, per recent legislation changes documented by the IRS. That’s a government-mandated withdrawal schedule that dictates your tax timing later on.

Setting up a Self-Directed IRA (SDIRA) is where the real rate variations happen, but buckle up. You can invest in things like real estate or private debt, which means the “rate of return” can swing wildly from potentially high double digits to losing everything. However, you usually pay significantly higher administrative fees for SDIRA custodians, often involving flat monthly or annual fees that could run you $150 to $300 just to hold the account open, regardless of your balance.

That administrative fee structure is the big downside I always point out. If you only have $5,000 in your IRA, paying a $150 flat fee is nearly a 3% drag on your portfolio before you even make a dime. For smaller investors, a platform that charges zero maintenance fees, even if their cash sweep rate is slightly lower, is almost always the better deal. I once saw a tiny brokerage charge $5 per transaction for non-standard assets within an SDIRA, and I thought, “Who uses this service?” It felt predatory for anyone not dealing with massive institutional flows.

If you’re looking at a Traditional IRA, the key “rate” consideration is your current marginal tax bracket versus your expected bracket in retirement. If you’re in a high earning year now, say over $150,000 filing jointly, taking the immediate tax deduction saves you real money today, betting you’ll be in a lower tax bracket when you pull the funds out decades from now, as detailed by advisors over at Investopedia.

Ultimately, the best rate for your IRA is the one that keeps you invested consistently without nickel-and-diming you out of small balances, which usually means the big three discount brokers. But honestly, when you look at how much money we’ll all need to save to fight inflation, worrying about which brokerage gives you an extra $5 in interest on idle cash seems utterly pointless.