Bridge Loan Interest Rates: Short-Term Financing for Property Transitions

Seventy thousand dollars is what I ended up paying just to keep the lights on while waiting for my primary mortgage to close on that fixer-upper in Scottsdale. That staggering six-figure swing taught me everything I know about bridge loans. You need one when time is the villain, usually when you’ve found the perfect new pad but haven’t sold the old one yet. Think about the logistics: you’re buying one property, selling another, and juggling closing costs simultaneously. It’s a tightrope walk, and the bridge loan acts as the safety net, albeit an expensive one.

These things aren’t for the faint of heart or light of wallet. They are inherently short-term financing, designed to span a gap, meaning you’re paying a premium for speed and flexibility. Most lenders cap the term at around 12 months, though you can sometimes stretch it to 18 months if you negotiate hard and your equity position is rock solid. If you miss that repayment window, well, things get ugly fast, probably involving foreclosure proceedings on one of your assets—nobody wants that headache.

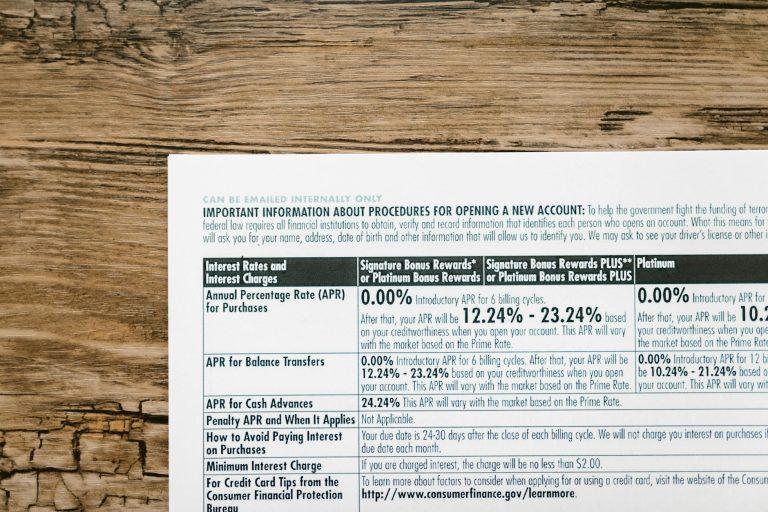

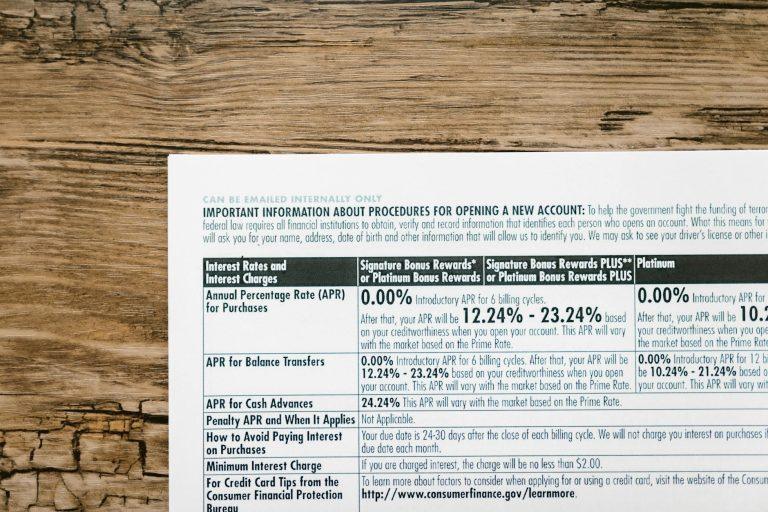

I remember talking to my broker about one particularly aggressive builder who quoted me an interest rate that felt criminal, something north of 14% APR, plus those hefty upfront origination fees that can easily hit 2% to 5% of the loan principal. You have to look at the whole package. A lower stated rate might hide massive points, and conversely, a huge upfront fee means less cash to cover immediate repairs on your new house. It’s a vicious balancing act, frankly.

The allure, of course, is speed. When you present an offer using a bridge loan to finance the purchase, sellers treat you like royalty compared to the standard buyer who needs 45 days to line up their financing contingent. We saw this clearly during the 2021 housing frenzy; sellers preferred a 30-day close contingent on a bridge loan over someone who might bail at the last second because their existing home sale fell through. That leverage is powerful, justifying some of the terrible interest rates you see listed on sites like Investopedia when they discuss temporary financing.

Here’s the big, ugly truth, the real limitation that nobody pushes hard enough: bridge loans are notoriously inflexible regarding property condition. If you’re buying a wreck that needs major structural repairs, securing that interim financing becomes nearly impossible unless you have enormous down payment capital or significant reserves. The lender needs to see clear, salable equity in both properties; they aren’t FHA loan programs for fixer-uppers. They’re specialized tools for people with excellent credit scores and assets already in hand.

My personal opinion? If you can avoid a bridge loan by staging the sale of your current home before buying, do it. Swallow the cost of temporary storage or renting an Airbnb for a couple of months. The financial maneuvering required to manage the dual mortgages and interest payments on a bridge loan is stressful enough to derail a marriage. I saw a friend in Denver nearly lose their shirt because the sale of their condo stalled for four months longer than anticipated due to slow permitting requirements, racking up thousands in extra interest payments.

The Loan-to-Value (LTV) ratio is crucial here, often needing to be kept conservatively low, maybe 70% or less across both properties combined, depending on the lender’s comfort level with your exit strategy. Lenders want assurance that if you can’t sell Property A quickly, they can foreclose on Property A swiftly and still recoup their money from Property B. You are providing security in the form of your existing assets, which is why established hard money lenders often dominate this space, not your local community bank. For a deeper look at how LTV impacts risk profile, checking out guidelines from the Consumer Financial Protection Bureau can give you a sense of the regulatory landscape surrounding these loans.

It’s shocking how quickly the closing costs add up when you factor in appraisal fees, legal costs, and the lender’s processing fees just for setting up this temporary accommodation. Honestly, the sheer administrative burden involved in signing papers for two synchronized closings made my head spin for about 72 hours straight.

So, you get the money, you close quickly, you get your new keys, and then you desperately pray the market doesn’t crash while you try to unload the old place within that nine-to-twelve-month window. If you’re using it to fund a flip, rather than buying a primary residence, the risk profile skyrockets because construction delays or permitting nightmares guarantee you’ll blow past that short repayment term. Trying to refinance a bridge loan into conventional financing at the last minute is a frantic, last-ditch effort that relies entirely on market conditions being favorable 10 months later.