The Business Loan Application Process Nobody Tells You About

I’m still a little amazed by how some banks operate when you’re trying to get a business loan. You think you’ve got all your ducks in a row, you submit what feels like your entire life history, and then… crickets. Or worse, a form rejection with no explanation. It’s a maddening experience, especially when your business is on the line.

When I was trying to secure a small business loan for my first venture, a small coffee shop, I swear I filled out the same information about my credit score and projected revenue five different times across three different applications. It’s like they don’t talk to each other internally! This whole application process can feel designed to weed people out, not assess their actual potential. We’re talking about hours, sometimes days, spent gathering documents: tax returns for the last three years, profit and loss statements, a detailed business plan, bank statements, and often a personal financial statement, too.

One of the biggest hurdles nobody really spells out is the sheer amount of documentation they demand. It’s not just about having good credit, though that’s obviously a big part of it. They want to see a clear, unwavering path to repayment, and that means dissecting your financial past, present, and future like a forensic accountant. Honestly, my biggest frustration came from the vagueness. You’d ask points of clarification and get stock answers that weren’t helpful at all. It’s nerve-wracking.

Of course, there are definitely upsides to this thoroughness. Lenders need to protect their capital, and a rigorous underwriting process helps them identify legitimate businesses with a solid repayment capacity. Think about it: if they just handed out cash to anyone, there’d be a lot more failed businesses and a lot less money flowing around for responsible entrepreneurs. SBA loans, for example, which are partially guaranteed by the government, still require mountains of paperwork but can offer better terms and lower interest rates because of that guarantee. You can learn more about different types of SBA loans on the official Small Business Administration website (https://www.sba.gov/funding-programs/loans).

The real kicker, though, is that even if you’ve got a fantastic business plan and impeccable credit, you can still get rejected. This happened to a friend of mine who was looking to expand his landscaping business. He had a solid track record, showed clear growth, and had the collateral to back a significant loan. But the bank perceived his industry as too “cyclical” and simply said no. It’s a subjective judgment call, and sometimes, despite your best efforts, the lender just doesn’t see your vision or feels it’s too risky for their particular risk tolerance at that moment. It’s a tough pill to swallow.

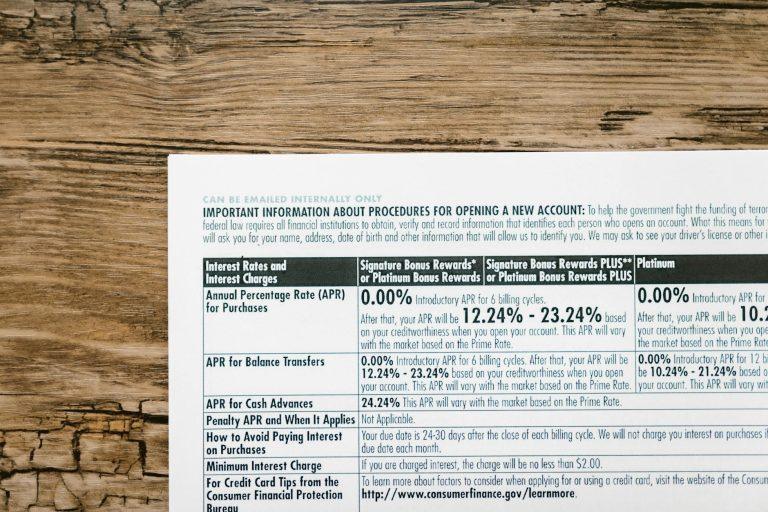

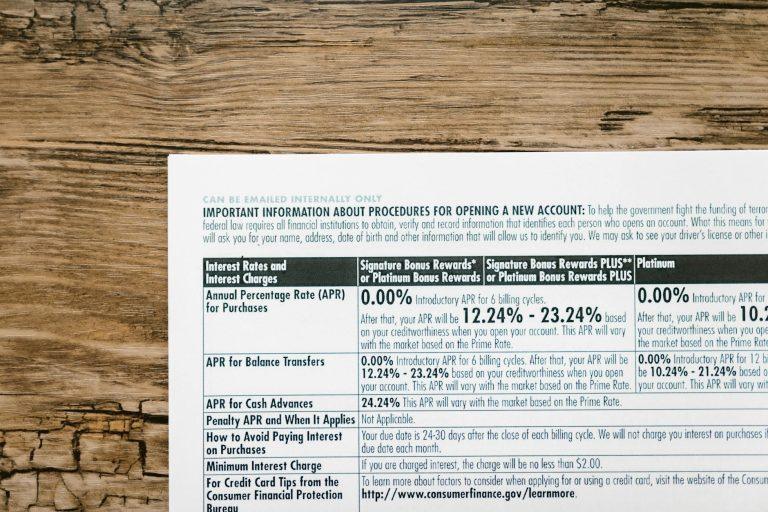

You’ll also find that the interest rates can vary wildly depending on the type of loan, the lender, and your financial profile. A term loan from a credit union might have a decent rate, say around 5-10%, while a merchant cash advance could have effective interest rates well over 30%, sometimes even 50%. Always, always shop around. Places like NerdWallet have great tools for comparing loan offers (https://www.nerdwallet.com/business-loans).

And don’t even get me started on the fees. There are origination fees, application fees, appraisal fees, and sometimes even prepayment penalties if you decide to pay the loan off early. These additional costs can add up quickly, sometimes adding several percentage points to the overall cost of borrowing. It’s why reading the fine print on that loan agreement is absolutely crucial, something many people sadly skim over.

For a moment, I thought I’d never get approved for anything. The application process felt like being interrogated by a committee with a crystal ball, trying to predict the future of my business with absolute certainty. The wait times between submitting documentation and getting a response can stretch for weeks, sometimes a couple of months depending on the financial institution and the loan’s complexity. It’s a perfect breeding ground for anxiety.

What’s truly baffling is how often the loan denial is a result of the lender’s internal policies or market conditions, rather than a fundamental flaw in your business. Imagine pouring your heart and soul into a business loan application, only to be told no because the bank’s loan portfolio is already “full” in your sector. The website Investopedia breaks down common reasons for loan rejections (https://www.investopedia.com/terms/l/loan-application-denial.asp), which can be a helpful, albeit depressing, read.

Ultimately, the business loan application process is a gauntlet. It’s designed to be difficult, and that’s not always a bad thing, but the lack of transparency and the sheer amount of hoops to jump through can feel downright absurd. Sometimes, the best business loan is the one you don’t end up needing.