The Impact of Credit Score on Interest Rates You Qualify For

Man, when I first bought my beat-up Honda Civic back in my early twenties, I thought my credit score was just some arbitrary number someone made up to annoy me. I got approved, sure, but the interest rate they slapped on that loan was outrageous—I think it was hovering around 14%! That’s the painful real-world impact we’re talking about: the difference between a good score and a bad one can cost you thousands over the life of a loan.

A score in the mid-800s, on the other hand, gets you access to the velvet rope section. Lately, I’ve seen mortgage offers coming in for folks with excellent credit where the Annual Percentage Rate (APR) is less than half of what I paid for that ancient Honda. We’re talking about potentially saving tens of thousands of dollars on something major like a thirty-year mortgage, just because your payment history is clean. It’s purely insane how much power resides in those three digits.

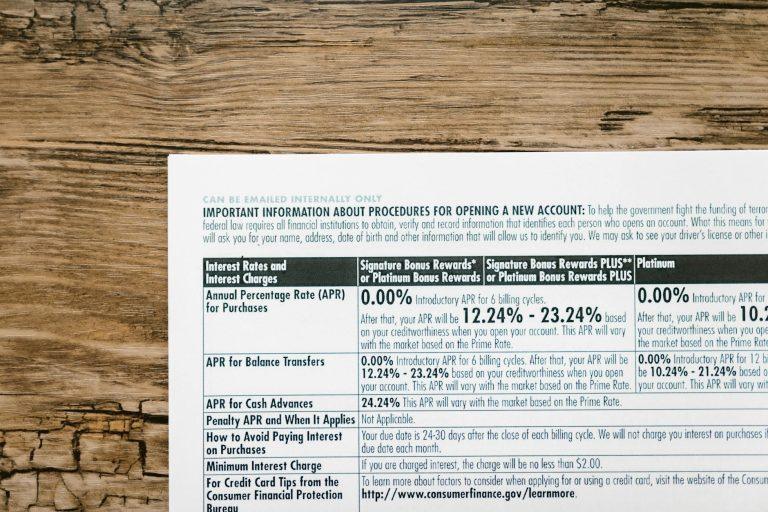

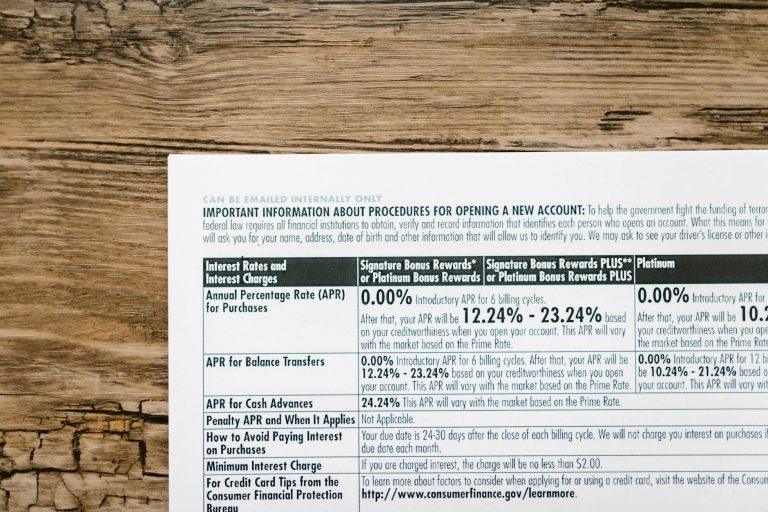

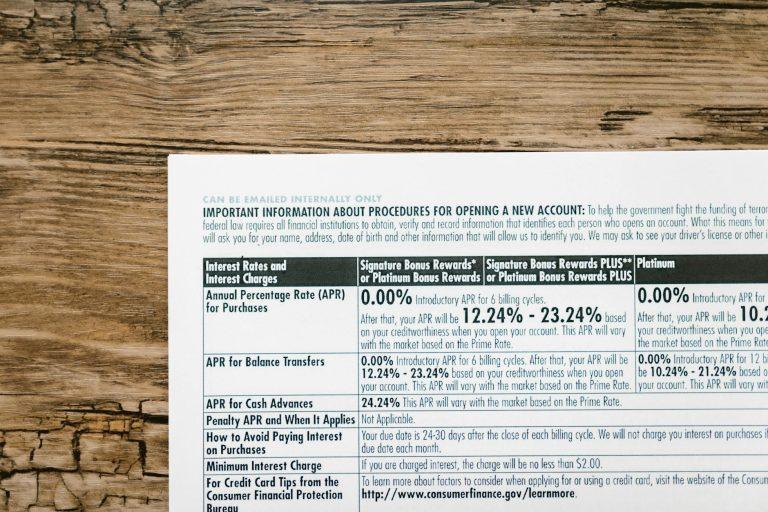

You see this most obviously with credit cards too. If you’ve been juggling payments successfully for years, you might snag a card offering 0% introductory APR for 15 months, which is practically free money if you’re smart about paying it off. If your FICO score is languishing in the low 600s, you aren’t seeing those offers; you’re getting stuck with cards that carry an APR of 29.99%, making carrying a balance virtually pointless.

The biggest sticker shock comes when you consider auto loans or personal loans, especially when you’re borrowing a significant chunk of cash. Think about a $30,000 loan over five years. A person with a prime score (say, 740 or higher) might get an 8% rate, while someone with a subprime score (below 620) could easily be quoted 18%. That difference, according to data from places like Investopedia, translates to paying back almost an extra $7,000 just in interest charges. That’s seven grand evaporated because of past financial behavior.

I remember trying to get a decent rate for a small business loan a few years back. My business credit was solid, but my personal credit utilization ratio had spiked temporarily because of an unexpected medical bill. The loan officer looked at my file, sighed heavily, and said the best they could offer put me about 2 percentage points higher than the initial quote. It was a real demonstration of how interconnected these different credit profiles can be, and honestly, I was furious they couldn’t look past a temporary blip. Transparency in how lenders weigh these factors is often lacking.

When you’re shopping around for rates, remember that there are different models out there, like the VantageScore versus the standard FICO. Lenders don’t always use the same yardstick, which means your score might look slightly different depending on where you pull it from—a concept many folks find confusing, as detailed by NerdWallet. Always check which scoring model your potential lender typically uses if you want the most accurate pre-qualification feeling.

One actual limitation you have to chew on is that even with a perfect 850 score, you aren’t guaranteed the absolute lowest rate advertised. Those rock-bottom public offers you see on commercials often require you to meet incredibly stringent criteria beyond just the score itself, such as having a super low debt-to-income ratio or putting down a huge down payment on a house. The lowest published interest rates are usually reserved for the absolute statistical elite.

It’s not just about loans, either; your score impacts insurance premiums in many states these days. Companies use something called an insurance score, which is highly correlated with your credit history, to assess risk, meaning even if you’re paying cash for everything, a poor score can quietly increase your car insurance bill by 10% or 20% annually. You can check official guides outlining this practice on government sites like the Federal Trade Commission (FTC).

Ultimately, building a strong credit profile is like preparing for a long road trip; you pack the essentials, check the fluids, and hope for smooth sailing, but sometimes the road just decides to throw a massive pothole right in front of you. I find it deeply ironic that we have to bribe lenders with years of good behavior just to get permission to borrow our own money back at a reasonable price.