Credit Union Rates vs Banks: Where Members Get Better Money Returns

I remember the first time I seriously compared my checking account interest rate at a big national bank to what my local credit union was offering. I was staring at 0.01% APY on literally thousands of dollars sitting there, basically collecting dust, while my buddy, who banked at the credit union down the road, was pulling in closer to 0.50% APY on his savings. It felt like I was being actively penalized for not knowing any better.

You hear all the time that credit unions are way better for the consumer, and often, that’s absolutely true, especially when it comes to savings rates and loan rates. Since they’re non-profit, member-owned cooperative institutions, their whole mission isn’t generating massive shareholder profit; it’s serving the people who actually use their services. Think about that fundamental difference in structure—it has to affect the bottom line you see in your account statements versus what you see in a big bank’s quarterly report.

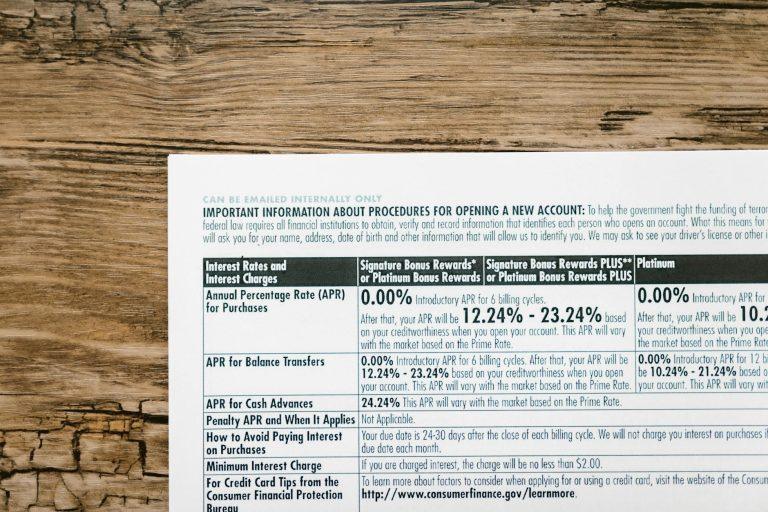

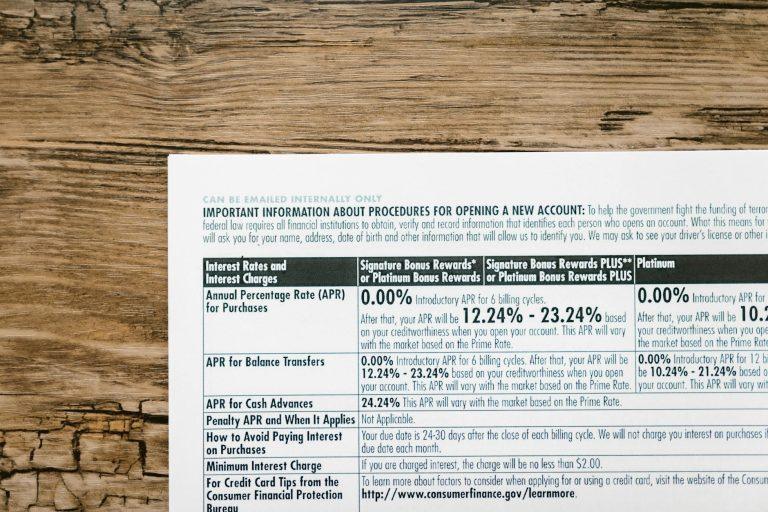

When we look at things like Certificates of Deposit (CDs), the difference can be startling. I watched one regional credit union offer a 1-year CD yielding around 4.75% APY last year, while the big players—the ones you see plastered on every highway billboard—were hovering closer to 4.00% or sometimes even lagging below that, depending on the minimum deposit required. That 0.75% difference on just a five-figure deposit translates into real, tangible money you get to keep.

But here’s where things get complicated, and you can’t just paint everything with the same broad brush. Getting access to those better rates often means dealing with significant inconvenience. You might find that amazing high-yield checking account at a small, hyper-local credit union that only has two physical branches in a tiny radius. If you travel a lot, or if you simply need to walk into a physical location after 5 PM because your schedule only allows it, you’re suddenly paying for that higher rate with your time and logistical headache, forcing you to rely heavily on ATMs or sometimes outdated online banking platforms.

I have to say, my personal experience is that the mobile banking apps at smaller credit unions are frequently a total disaster area compared to what a massive institution like Chase or Wells Fargo throws at you. Sometimes they feel about ten years behind technologically; logging in can be clunky, alerts are slow, and simple tasks like remote check deposit often fail on the first try. It really can be a source of genuine, low-grade frustration every single week.

For loans, the disparity usually runs in your favor at the credit union too. If you’re shopping for an auto loan, you’ll often see the credit union offering rates half a percent or sometimes even a full percentage point lower than the national average quoted by commercial banks. This is because they often use simpler, less costly underwriting models since they already know the customer base. You can usually check out generalized comparisons on sites like NerdWallet to see how this typically plays out across different loan types.

One serious limitation, though, is access to sophisticated services. If you’re a small business owner running a multi-million dollar operation that needs complex things like lines of credit, international wire transfers handled easily, or access to highly specialized treasury management tools, you’re probably going to have to stick with a major commercial bank. A small credit union simply doesn’t have the infrastructure or capital reserves to support those intricate corporate needs; they serve individuals and smaller member groups really well, which is why organizations like military branches or teaching hospitals often have their own dedicated credit unions.

It’s also crucial to check the depositor insurance. Both types of institutions are insured, but the names are different. Credit unions are insured up to $250,000 per depositor by the National Credit Union Administration (NCUA), which is functionally identical to the FDIC insurance that protects bank deposits. Don’t sweat that difference, but do verify that institution is indeed covered by the NCUA before you park your life savings anywhere; the NCUA website has tools for checking this status.

So, if you’re someone focused purely on maximizing the interest earned on your emergency fund or getting the best possible rate on your first mortgage, the credit union is usually the clear winner, provided you can tolerate the slightly less polished user interface. Frankly, for the average consumer putting away a few grand for a rainy day, the extra tens of dollars they earn annually in interest probably outweighs the minor frustration of a slower app experience.