The Loan Terms You Should Never Agree To (But Probably Will)

I remember taking out my first car loan. I was so excited to drive off the lot, I barely glanced at the paperwork. Big mistake. There are definitely loan terms you should absolutely steer clear of, even if the salesperson makes it sound like the deal of a lifetime. You’ve got to protect yourself from getting trapped in something you can’t afford down the road.

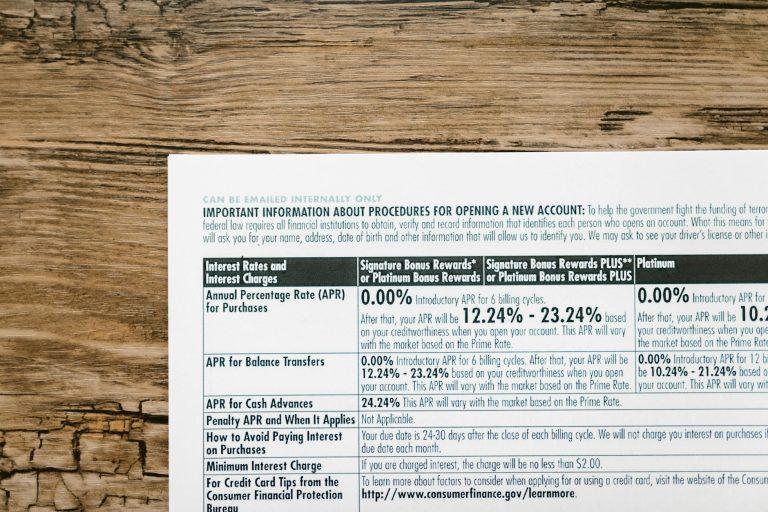

That interest rate? You don’t want it creeping up unexpectedly. Variable interest rates sound okay at first because they might start lower. But here’s the kicker: that rate can go up and up, making your monthly payments skyrocket. I saw a friend get burned by this on a personal loan; what started as a manageable payment ballooned into something way more than she budgeted for. Always look for a fixed interest rate. It’s predictable. You’ll know what you owe every month for the entire life of the loan. It’s just a more secure feeling, honestly.

Fees. Oh, the fees! Seriously, there are so many hidden fees that can nickel and dime you to death. Think about origination fees, which are basically charges for processing your loan. Sometimes these can be a percentage of the loan amount, adding a chunk to what you actually borrow. Then there are prepayment penalties. This is wild, but some lenders will charge you extra if you try to pay off your loan early. Why would they do that? Because they want to make sure they get all the interest they planned on. It’s infuriating! You’re trying to be responsible and get out of debt faster, and they’re trying to punish you for it. It doesn’t make any sense in the real world.

Don’t agree to a loan term that has a ridiculously long repayment period, like 10 or 15 years for a personal loan or even a car. Sure, your monthly payments will be lower, which sounds good. But over that extended period, you’ll end up paying way, way more in interest. It’s like stretching out a small pain over a decade instead of a few years. Imagine borrowing $20,000 and ending up paying back $35,000 or more because of a 15-year loan term. Ouch. Unless you absolutely have no other choice, avoid these extended terms.

Another big red flag is a balloon payment. This is where you make smaller payments for a while, and then BAM!, a huge lump sum payment is due at the end. It’s a nasty surprise waiting to happen. People often can’t afford that massive final payment, and then they’re forced to refinance, often at worse terms. It’s a desperation move for lenders, and you never want to be in that position. The Consumer Financial Protection Bureau (CFPB) has a lot of great, no-nonsense information about avoiding predatory loans and understanding these terms.

Then there’s the sheer lack of transparency. If a lender is cagey about explaining the terms, or if the loan agreement is an inscrutable wall of legal jargon that even a lawyer would struggle with, walk away. A legitimate lender wants you to understand what you’re signing. Check out resources like Investopedia for breakdowns of common loan terms, so you’re not going in blind.

Just because the bank or dealership is offering it doesn’t mean it’s a good deal for you.

You’ll likely encounter these kinds of predatory terms when you’re applying for payday loans or certain title loans. These are often a last resort for people in a bind, and the terms are brutal. A payday loan might look like it’s only for a few weeks, but the annual percentage rate (APR) can be in the hundreds of percent. That’s not a loan; that’s a debt trap. Even with a legitimate mortgage, you need to be careful about adjustable-rate mortgages (ARMs) and understand how rate caps work. NerdWallet has helpful guides comparing different types of loans and their potential pitfalls, like this piece on understanding mortgage ARMs.

Seriously, don’t just sign the first thing put in front of you. Read everything. Ask questions. If something feels off, it probably is. You’re better off walking away from a loan offer than getting into something that will cripple your finances for years. Honestly, agreeing to a loan with a prepayment penalty is like agreeing to pay extra for the privilege of leaving a party early.