Why Paying Just the Minimum Is Keeping You Broke

I swear, I almost lost my mind the other day when someone told me they were only paying the minimum payment on their credit cards. It’s like they don’t realize they’re digging themselves into a deeper hole with every swipe. Paying just the minimum, that tiny amount that barely covers the interest, is financial sabotage. Your credit card company loves this strategy because it means you’ll be paying them interest for what feels like forever.

Think about it realistically. If you have a $5,000 balance on a card with a 20% APR and you only pay the minimum, which might be around $100, you’re actually sending a huge chunk of that $100 straight to the interest charges. That leaves a pittance to actually chip away at the principal balance. You could end up paying thousands of dollars in interest over several years, sometimes even decades, before you finally get the debt paid off. It’s a cruel, almost hidden fee for the privilege of being in debt.

This isn’t some abstract concept; I’ve seen friends go through this. My buddy, Mark, was in this exact situation with a couple of credit cards. He was making what he thought were responsible payments, but his balances just wouldn’t budge. He was feeling so overwhelmed, constantly stressed about money. It wasn’t until he sat down and really looked at his statements, calculating how much of his payment was just going to interest, that he understood the gravity of it. He was shocked by how long it would take to get out of debt and how much extra money he was essentially throwing away.

The real kicker is how easy it is to fall into this trap. You see that minimum payment amount, and it feels manageable. It’s a small number compared to the total balance, and it lets you keep that credit card open to use again, which is exactly what these companies want. They make their money on the interest, and people paying only the minimum are their golden geese. It’s a cycle of debt that’s incredibly hard to break free from once you’re caught in it.

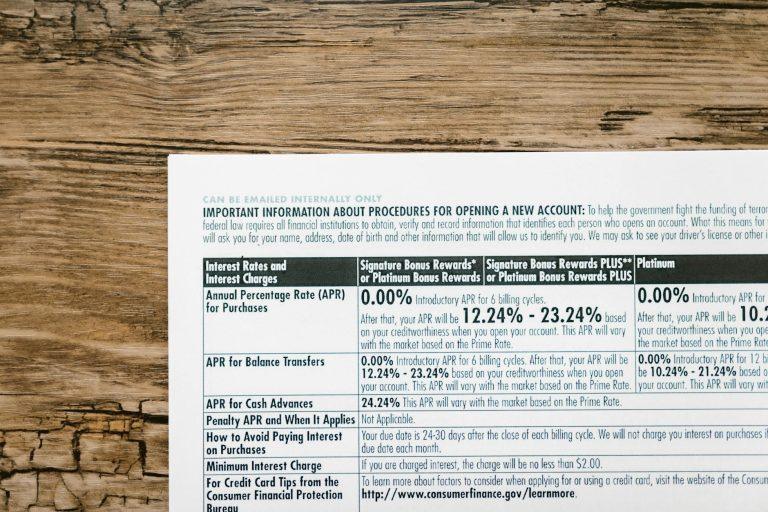

Honestly, some of these credit card companies are downright predatory with how they structure their minimum payments. They’ll put that minimum balance due in a large, bold font on your statement, almost daring you to pay only that. Meanwhile, the full amount due or a suggested payoff amount is in tiny print somewhere else. It’s a sneaky way to keep you paying interest for longer. According to articles from places like NerdWallet, paying only the minimum on a typical credit card debt could take over 10 years to pay off and cost you more than double the original amount in interest.

Here’s the infuriating part: making even a slightly larger payment than the minimum can drastically cut down the time it takes to pay off your debt. Let’s say you add just an extra $50 or $100 each month. Suddenly, that $5,000 balance with the 20% APR might be gone in 6-7 years instead of 10+ years, and you’d save thousands of dollars in interest. It’s not a magic trick; it’s just basic math, but the impact is huge. My cousin Sarah started doing this, and she was absolutely floored by how much faster her credit card balances were shrinking.

The downside, of course, is that paying more than the minimum means you have less disposable income in your pocket right now. If you’re already struggling to make ends meet, that extra $50 might feel like a lot. It requires budgeting and sometimes making tough choices about where your money goes. It’s not always a simple solution, especially for folks living paycheck to paycheck. A survey by the Consumer Financial Protection Bureau found that a significant percentage of consumers are struggling to pay more than the minimum, highlighting the widespread nature of this financial challenge.

Ultimately, viewing that minimum payment as anything other than the absolute worst-case scenario is a mistake. It’s designed to keep you paying interest, not to help you get debt-free. If you actually want to improve your financial situation and stop being broke, you need to commit to paying more than the minimum, ideally the full statement balance. It’s about taking control, not just making the smallest possible payment.

I’m pretty sure my neighbor still thinks paying the minimum is a smart way to manage his credit cards because it keeps his credit score from dipping due to late payments.