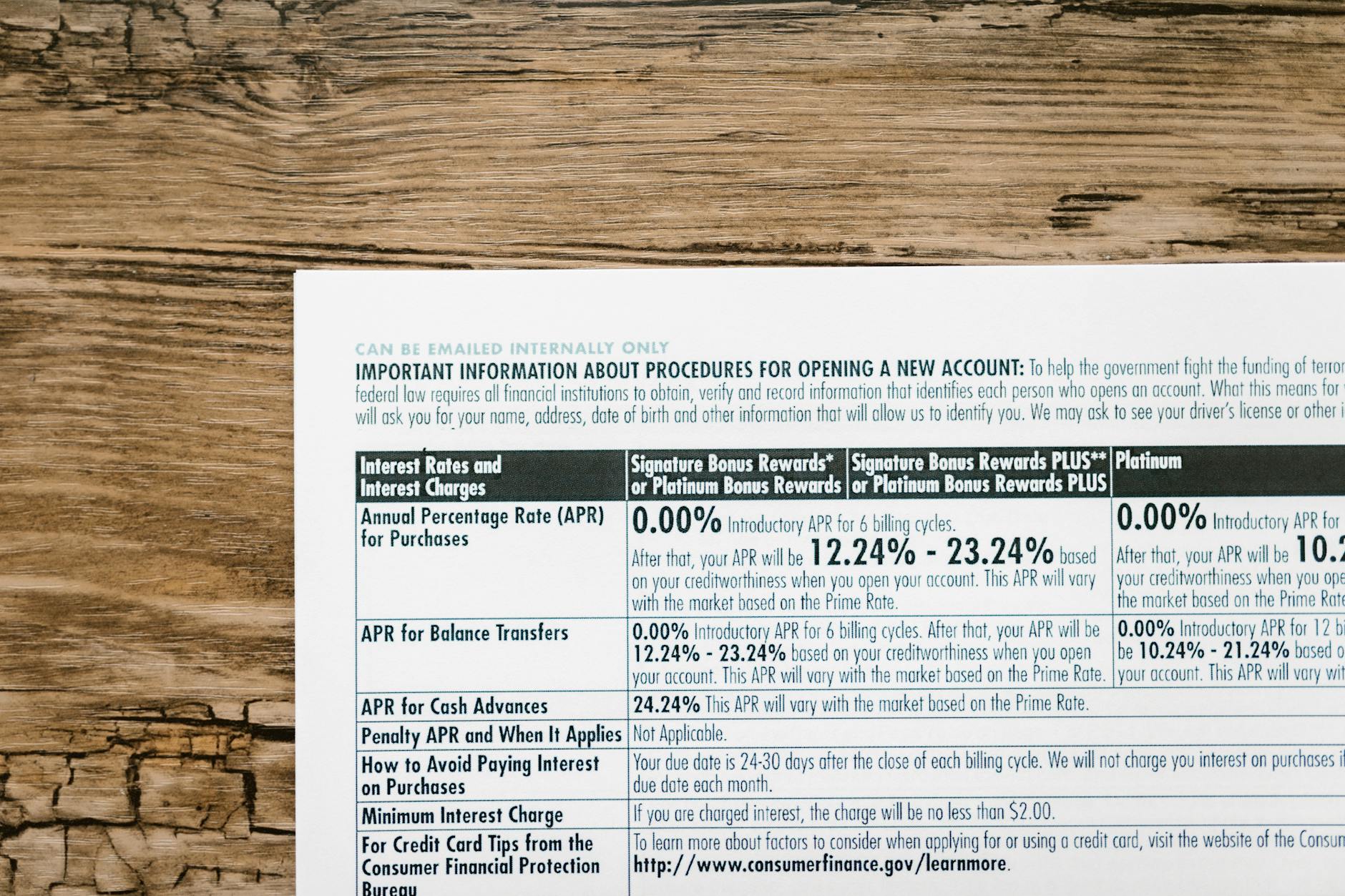

How I Negotiated My Interest Rate Down After Approval

I remember sweating bullets a few years back after getting my initial mortgage commitment. The rate they offered felt just a little too high, hovering around 5.5% for a 30-year fixed. I wanted that lower number, the one I’d seen in my hypothetical spreadsheets, but the bank seemed pretty firm once the underwriting was done.

You wouldn’t believe the amount of paperwork they throw at you once they say yes. It’s an avalanche of disclosures and figures. My biggest realization was that approval doesn’t actually mean the deal is sealed at the first rate quoted; it means you’ve passed their initial sniff test. The real negotiation happens in the window between conditional approval and locking that final rate, which can sometimes be 30 to 45 days.

My first tactic, which I genuinely believe works if you have competitive offers, was simply leveraging other lenders. I had a pre-approval from a local credit union sitting there at 5.25%. I walked into my primary bank, the one offering the 5.5%, printed out that other loan estimate—the one showing the lower rate—and slid it across the desk to my loan officer, Sarah. I didn’t make it a threat; I framed it as, “Hey, this other group is offering me this. Can you help me justify staying here?” It cost me practically zero dollars to deploy this strategy.

It’s baffling how often people just accept the first number thrown at them, especially when they’ve already invested so much time in the application process. People suffer from sunk cost fallacy here; they think, “I’ve already done all the work,” and they just roll over. I certainly felt that pull toward complacency.

Sarah actually gave me a little static at first, saying their cost of funds was higher, which is a classic line. But because I brought in that hard data from the credit union, she went back to her manager. She came back about three hours later—and this is where the surprise came in—she managed to shave two-tenths of a percent off, landing me squarely at 5.3%. I was shocked they’d move that much just because I held up a piece of paper from a competitor! This is often easier for mortgage brokers to manage than direct bank loan officers, who might have stricter overlays. For more on how competing offers impact your final loan terms, you might want to check out some of the analysis over at Investopedia about mortgage shopping.

Another crucial thing you can negotiate, which isn’t the rate itself, is the origination fee. Banks often hide legitimate room for movement there. My closing disclosure showed a $1,200 processing fee. I asked directly, “Can we reduce or waive this fee since we are locking in a rate that is slightly higher than the absolute lowest advertised market rate?” My rationale was that if they wanted my lender fees to be competitive, trimming the front-end costs was an easy way to sweeten the pot without affecting their ultimate yield percentage much.

They knocked $500 off that fee, straight up. Suddenly, the entire deal looked much better, even if the rate was only slightly improved. It was like finding money under the couch cushions, except I had to ask for it. Frankly, I think banks build the flexibility to drop points or fees into their initial quote structure specifically for seasoned negotiators or people who bring proof of other offers.

The real downside to this whole process is the timing pressure. If you keep shopping aggressively after getting that initial approval, you risk that the market shifts slightly, or your initial loan estimate expires, forcing you to requalify under worse terms. I had to move fast once Sarah gave me the 5.3% confirmation, locking it in within 24 hours before interest rates spiked again, which they tend to do annoyingly often. It’s a tightrope walk between getting the best deal and potentially losing the loan entirely, which, according to data from Fannie Mae, causes a significant portion of unstuck applications.

I learned that your borrower profile matters immensely too. Because my debt-to-income ratio was low—under 25%—and my credit score was up in the 800s, I had tremendous negotiating leverage. If you’re scraping by or have a few blemishes, they have far less incentive to move the price for you. My strong standing basically allowed me to apply pressure without immediate risk of them walking away.

So, while everyone tells you to shop around before applying, the real magic happens when you use those other competitive offers as ammunition after you’ve proven you’re a financially sound borrower capable of closing. It turns out that being a low-risk borrower permits you to be a high-annoyance requestor.