The Pre-Payment Penalty Clause That Trapped Me in a Bad Loan

That pre-payment penalty clause could’ve cost me thousands. I learned this the hard way with a personal loan I took out a few years back for some unexpected home repairs. It was for about $15,000 to fix a leaky roof and a busted water heater, and the interest rate seemed okay at the time, maybe 7%. I figured I’d pay it off quicker than the five-year term they laid out.

Boy, was I wrong. About a year and a half in, I got a promotion at work, which meant a nice raise. I immediately thought, “Great! I can knock out this loan and save on interest.” So, I calls up the bank, ready to hand over a lump sum to pay off the remaining $10,000 or so. Then they drop the bomb: a pre-payment penalty.

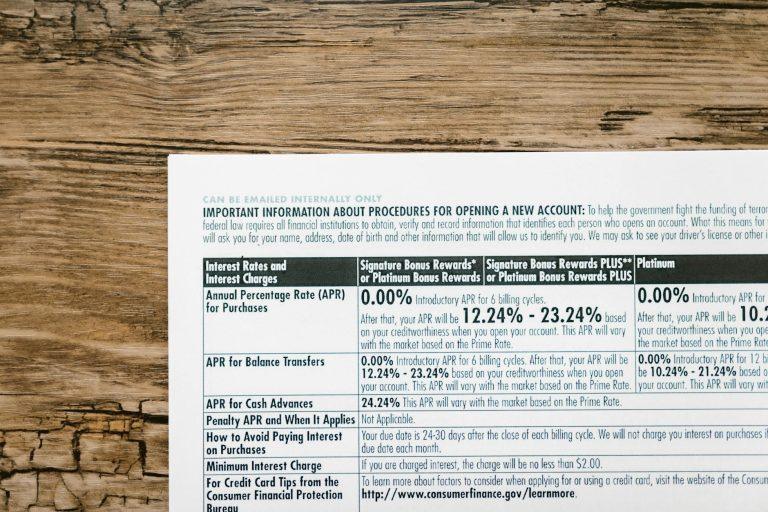

Apparently, this particular loan contract had a clause stating I’d owe 6 months of interest on the remaining balance if I paid it off early. Six months of interest on $10,000 at 7%? That’s a pretty chunk of change, like $350 right there, which totally negated the benefit of paying it off early. I was so mad, I almost hung up the phone. It felt like a total bait-and-switch, trapping me into paying more than I wanted to.

This is honestly one of the most frustrating things about some loan agreements. They make it sound like you have options, like you’re in control, but then they hit you with these hidden fees. It’s like they want you to stay in debt. You see these loan calculators online that show you how much you save by paying extra, but they don’t account for a lender actively penalizing you for doing just that.

The real kicker? I’ve seen this in a bunch of places. Car loans, sometimes even mortgages, though those are usually structured differently with refinancing costs. But for smaller personal loans, that pre-payment penalty can be a real sting. It’s not always obvious when you’re signing on the dotted line, especially if you’re in a rush or don’t fully understand all the legalese. I read the fine print that time, but honestly, I breezed over that section because I was just focused on getting the money to fix my house.

My advice? Always, always, always ask about pre-payment penalties before you sign anything. Don’t just skim. Ask for clarification. Some lenders are perfectly fine with you paying extra or paying off the loan early with no strings attached. For instance, many credit unions are known for having more consumer-friendly terms than large national banks. A quick search on NerdWallet’s guide to personal loans can give you a general idea of what to expect, but your specific contract is key.

Honestly, I ended up just sticking to the original payment schedule on that loan, which was agonizing. It took another year and a half to finally be free of it, and I know I paid more in total interest than I would have if I could have paid it off when I got that raise. It’s a tough lesson on the importance of scrutinizing every single line item. You can read all about how loan terms work on Investopedia, but nothing beats direct questioning.

And just when you think you’ve dodged the bullet, you’ll find another lender with a slightly different, but equally annoying, fee structure – maybe it’s a late payment fee that’s absurdly high or an origination fee that eats into your loan amount. It’s a constant battle to find a straightforward deal. For example, a 2023 report from the Consumer Financial Protection Bureau highlighted how common hidden fees are across various financial products. Even government-backed loans, like FHA loans on the HUD website, have their own complexities you need to understand.

Ultimately, that loan taught me that sometimes the best way to get out of a bad deal isn’t to pay it off early, but to simply wait until the contract naturally expires, even if it means paying more interest in the long run.