Prime Rate Changes: How Banking Rates Affect Your Borrowing Costs

I remember back in 2008 watching my credit card interest rate jump like a startled cat; it was honestly terrifying for someone just starting out with their finances. That sudden shift hammered home how powerfully the prime rate dictates what you actually end up paying for debt. Most people think the prime rate is just some abstract banking term, but it’s the real-world foundation for just about every variable-rate loan you have, from your home equity line of credit (HELOC) to that fancy personal loan you took out last year.

A bank setting the prime rate is basically announcing the absolute lowest interest rate they’re willing to offer their most creditworthy corporate customers. You’ll almost always see it quoted as being 3% above the Federal Funds Rate target range set by the Federal Reserve. When the Fed hikes rates—which they’ve been doing a lot of lately—banks immediately follow suit, usually within a day or two, and boom, your monthly payment goes up.

This whole mechanism is usually transparent, but sometimes banks are a little slow to decrease rates when the Fed drops them, and that really bugs me. It feels like they’re perfectly happy to boost your costs instantly but take their sweet time passing along actual savings. You’ve got to keep an eye on your loan disclosures, because that prime rate tied to your credit cards or variable-rate mortgages is what matters most for your monthly budget. Apparently, according to Investopedia, this relationship is codified, but enforcement sometimes feels loose.

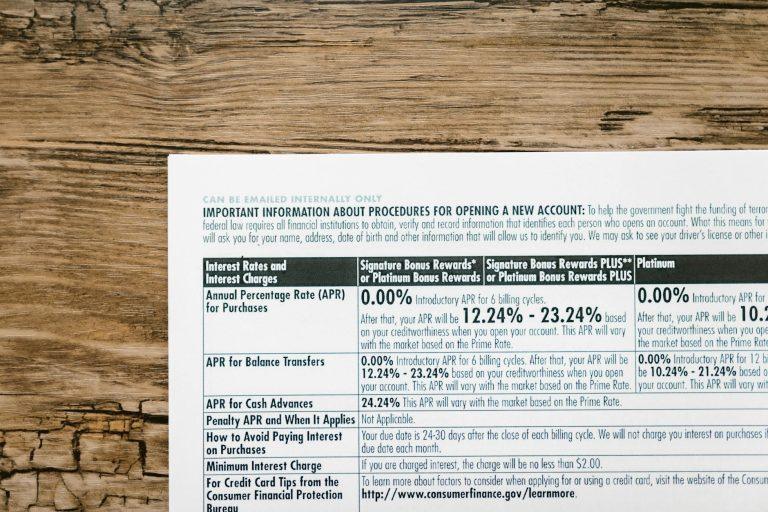

When someone looks at their credit card statement and sees their APR sitting right around 22% or maybe even flirting with 30% these days, that number is almost entirely built on the current prime rate plus their specific margin. If the current prime rate is, say, 8.5%, and your card has a prime + 20% structure (which is rare, but happens in super high-risk scenarios), you’re paying dearly. More common is Prime + 14% or similar.

Owning a home with an adjustable-rate mortgage, or ARM, makes you acutely sensitive to these movements. I have a friend whose payment on their jumbo ARM jumped by nearly $300 a month over the last eighteen months just because the Fed kept tightening policy. It’s not pennies; it’s serious money altering people’s capacity to afford their housing.

The main frustration with how the prime rate trickles down is how it impacts secured lending, too. Think about small businesses relying on revolving business lines of credit. They use these lines to manage short-term cash flow, buying inventory before a big sales season. If the underlying cost of capital—driven by the prime rate—spikes too quickly, those businesses might have to delay hiring or skip restocking altogether. I saw a local bakery nearly pull the plug on an expansion plan because their line of credit rate suddenly climbed two percentage points in a single quarter; they just couldn’t justify the risk anymore.

For borrowers, the biggest downside here is the lack of control; you can shop around for the best credit card offer or the best mortgage lender, but you can’t negotiate the prime rate itself. You’re subject to macroeconomic policy decisions made far away in Washington D.C. For instance, while the Federal Funds Rate is heavily influenced by the Federal Reserve’s dual mandate (managing inflation and employment), the resulting prime rate is often adjusted irrespective of whether your local economic conditions warrant higher borrowing costs. You can check the historical movements on sites like the Federal Reserve Bank of St. Louis to see just how closely bank rates track those policy shifts.

So, when people talk about getting the “best rates,” they’re really just hoping to secure the smallest possible margin above the prevailing prime rate. That’s where your negotiating power lies, not in changing the baseline index itself. If you’re looking to lock in predictable costs, skip anything tied to the floating prime rate entirely and fight tooth and nail for a fixed-rate loan, even if the initial offer seems a little higher; peace of mind is worth something. Truthfully, having all my savings earning negligible interest while I pay through the nose on my debts feels like a systemic trick designed specifically to punish anyone who ever dared to borrow money.