Rate Comparison Tools: Finding the Best Financial Products for Your Money

Man, when I first started trying to sort out refinancing my mortgage a few years back, I felt like I needed a law degree just to compare interest rates. I spent a solid three weeks just wading through bank websites, all while these loan officers were calling me daily, talking about APR, origination fees, and whether I wanted to buy down the point or not. It was chaos, truly.

The promise of rate comparison tools sounds like heaven, right? You punch in your credit score and desired loan term, and bam, you get a clear side-by-side chart listing the best financial products for your money. That’s the dream version they sell you. In reality, things feel a little more… curated.

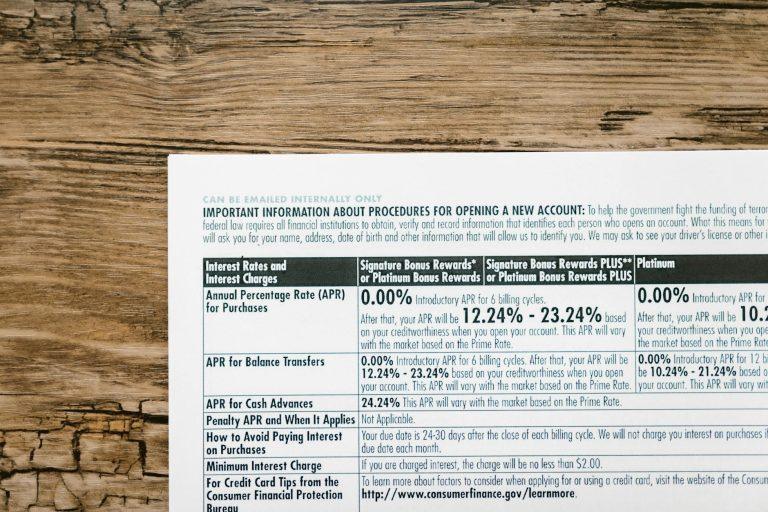

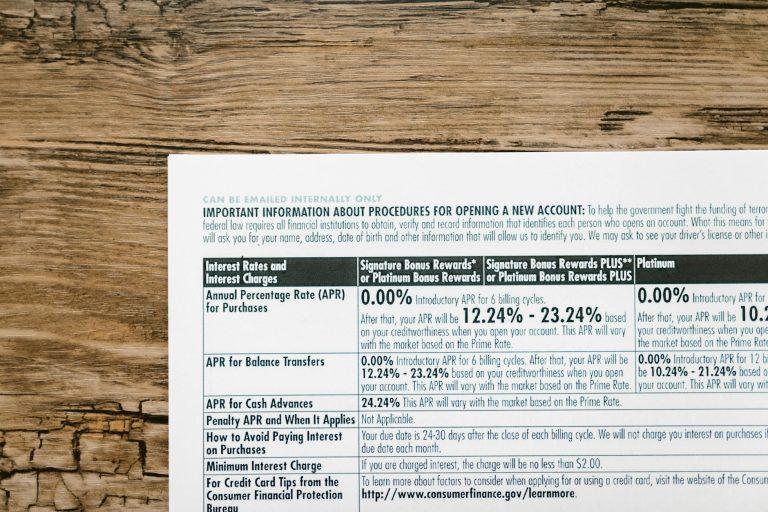

I remember one tool I used where they claimed to show live rates from dozens of lenders, but half the quotes I got back were clearly outdated or required a down payment so huge it was unrealistic for my situation. You have to remember these aggregators often have referral agreements, meaning the lender paying them the most might pop up first, potentially skewing your view of the absolute lowest rate available. It’s a business, after all; they aren’t just altruistic matchmakers.

Think about simple things like high-yield savings accounts (HYSAs). Tools like those offered by consumer sites like NerdWallet or Bankrate can be fantastic starting points. They often filter out the legacy brick-and-mortar banks that pay practically zero interest and point you toward online organizations offering yields sometimes 10 to 15 times higher. I moved my emergency fund after seeing one of these comparisons and realized I was leaving serious money on the table just by keeping it with my old regional bank that was paying less than zero point two percent.

But there’s a real sting in the tail when using these comparison engines for loans: rate locks. You see a fantastic 4.75% mortgage rate quoted online, which prompts you to apply immediately. Then, once the lender pulls your formal application and runs a hard credit check, the actual locked-in rate they offer you might jump to 4.9% because the market shifted slightly or they found something in your report they didn’t like on the initial soft pull. Dealing with that kind of volatility is incredibly frustrating.

Specific tools aimed at narrower finance categories can sometimes be better. For comparing credit cards, sites that let you filter purely by rewards structure—cash back versus travel points—are incredibly useful. You can immediately discard cards that offer great points if you only want simple flat-rate cash back, cutting your research time down from hours to about fifteen minutes. My buddy Mark, who travels a ton, uses one specific comparison site exclusively because it prioritizes airline partnerships for earning miles, ignoring everything else.

The biggest weakness, genuinely, is that these automated systems rarely account for the human element or the specific quirks of your financial profile. For instance, if you’re a self-employed independent contractor, most algorithms choke on accurately assessing your actual income stability, leading to generalized, less favorable pre-approvals. You often have to call a broker anyway to explain your messy P&Ls, completely negating the “instant comparison” benefit.

When navigating insurance, particularly auto insurance, you’ll find that some comparison sites are just lead generators selling your information to three or four major carriers. You don’t get broad market coverage; you just get the carriers who agreed to pay for that lead. For truly comprehensive insurance shopping, calling an independent local insurance agent who has access to dozens of smaller carriers often yields superior results, even if it feels old-fashioned.

So yeah, these comparison tools are essential time-savers for the initial filtering; they stop you from bathing in ignorance about current market standards for things like CD rates or car loan structures. But never, ever trust the very first number you see without verifying it directly with the underwriter before signing anything substantial.

The underlying architecture of these comparison platforms makes them inherently biased toward volume and standardized products, meaning the really niche, specialized financial products that might actually be better for a very specific consumer profile are usually invisible.