Rate Shopping Strategies: How to Find the Best Deals on Loans and Savings

Man, finding a good rate used to feel like pulling teeth. I remember trying to refinance my first mortgage, and the whole process took almost three months. I was getting quoted wildly different Annual Percentage Rates (APRs) from lenders who all claimed they were giving me their “best offer.” It was enough to make you just sign the first pre-approval you saw out of sheer exhaustion, which, naturally, is exactly what they count on.

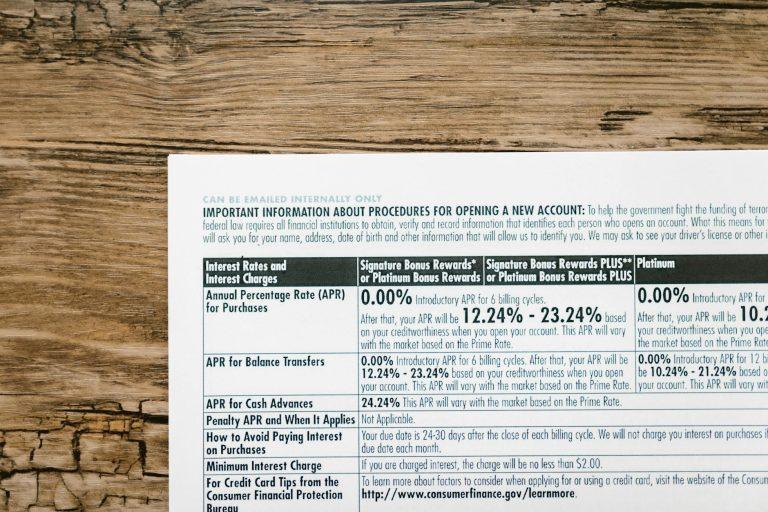

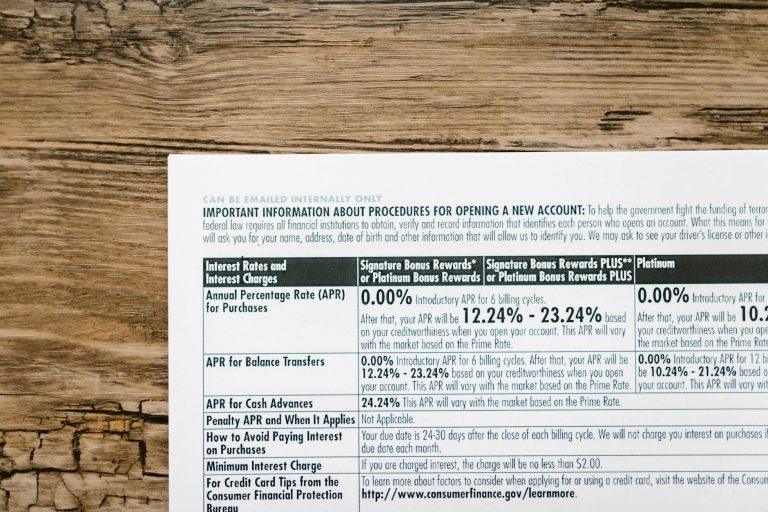

The biggest mistake people make when rate shopping is only looking at the headline interest rate. You really have to dig into the Loan Estimate document. I learned this the hard way when I secured a mortgage offer that looked fantastic on paper, but then the stack of origination fees and third-party charges added up to nearly $5,000 more than a competitor’s quote, even though their stated interest rate was 0.25% higher. That hidden cost changes everything, doesn’t it? Always focus on the total cost of borrowing, expressed through that APR.

For borrowing, you absolutely need to shop multiple types of institutions simultaneously. Don’t just stick to your big national bank. You should be checking credit unions—they often operate as non-profits and frequently offer significantly lower auto loan or personal loan rates, sometimes by one full percentage point compared to huge commercial banks. Also, don’t forget about online lenders like SoFi or LendingClub; they have lower overhead, which sometimes translates directly into better pricing for you. Check out what Investopedia says about comparing lender types for a good starting point.

When it comes to savings, the game is totally different, but the need for rate shopping is just as intense. Seriously, I check my High-Yield Savings Account (HYSA) rate perhaps monthly. If you’re letting your emergency fund sit earning 0.10% at a local brick-and-mortar joint in this economy, you are actively losing money to inflation, which is just infuriating to watch happen.

You need to look at online-only banks or fintech platforms offering HYSAs right now. They might advertise 4.5% APY or sometimes even push toward 5.0% during tighter monetary policy periods. That spread between earning almost nothing and earning a solid return over a year with $20,000 sitting there is substantial—we’re talking hundreds of dollars annually just by switching providers. For example, Ally Bank or Marcus by Goldman Sachs often compete fiercely in this space.

Here’s a piece of genuine frustration: the rate lock process is often a messy guessing game. You think you have a solid 30-day rate lock confirmed for your home purchase, then the closing gets delayed by an inspection issue, and suddenly your lender is slapping you with extension fees or worse, forcing you onto a floating rate that jumps up when you finally get to the closing table. It’s a prime example of how lenders protect themselves far more aggressively than they protect the borrower.

So, how do you actually execute this comparison effectively? For loans, gather at least three full, written Loan Estimates before making a decision. Don’t base it on verbal quotes alone. For savings, use comparison sites to see what the top five available APYs are this week, prioritizing accounts that are FDIC insured up to the standard $250,000. You can verify the insurance limits over at the Federal Deposit Insurance Corporation website.

My personal opinion is that for long-term products like mortgages, you should almost always accept a slightly higher upfront rate if it means avoiding predatory points or guarantee fees because those are harder to recover from. For short-term liquidity, like checking or savings, chase the highest APY you can find, regardless of the institution’s size; that money needs to work hard for you immediately.

The biggest limitation in this whole endeavor is the time commitment required. To truly maximize savings, you have to be prepared to move your cash every six to nine months because the top rates change constantly, and being lazy will cost you real money, but honestly, setting up those ACH transfers takes maybe ten minutes each time, so the friction is minimal compared to the reward. Yet, people still don’t bother.