Best Rates on Rewards Checking Accounts: Earn Interest Plus Cash Back

Man, opening a rewards checking account used to feel like trying to find a unicorn. You’d get some pathetic interest rate, maybe 0.01% APY, which wouldn’t even cover the cost of the ATM fee you paid last Tuesday. Seriously, I remember looking at my bank statement, seeing a whole two cents earned in interest over three months, and just shaking my head. That’s why I’ve spent ages digging into the options that actually pay you back for just using your money.

Surprising fact: Some of the best rates aren’t even from the giant brick-and-mortar banks everyone defaults to; they’re often tucked away at smaller credit unions or online-only operations. They can afford higher payouts because their overhead is way lower, unlike the massive chains that need to fund those fancy downtown branches.

You have to figure out what kind of rewards you actually want. Some accounts are all about bumping up your interest yield. Think about that high-yield checking account structure, where you might snag 3% APY or maybe even a hair more, but there’s always a catch, right? Usually, that catch involves things like making 15 debit card transactions a month or setting up multiple ACH direct deposits. It’s doable, but you gotta remember you’re actively managing your banking habits.

Cash back is the other side of the coin, and this is where things get interesting, though often more complicated. I saw one regional bank offering 5% cash back on grocery store purchases up to $$500$ a month. That sounds amazing until you realize they only code certain retailers as “grocery,” meaning Costco (where I do most of my shopping) often doesn’t count. That’s when the sheer absurdity of these rules hits you, and you want to throw your phone across the room.

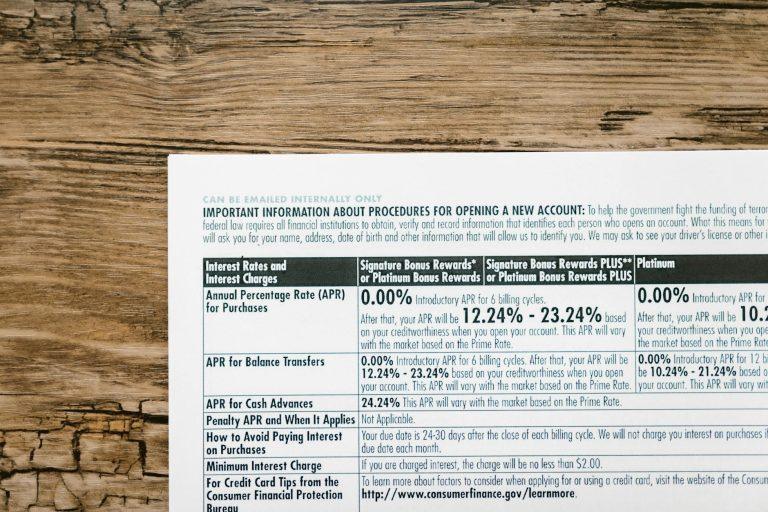

High-APY checking accounts frequently impose caps, and this is a real limitation you can’t ignore. Let’s say you find an account offering a juicy 4% APY, which is great for your emergency fund sitting there liquid. The shock comes when you read the fine print: the 4% only applies to the first $$10,000$ in your account. Anything above that earns squat, or maybe that rock-bottom 0.01%. If you have more substantial savings, this immediately tanks the overall return, making that advertised 4% look kind of silly. You’ll need to check out resources like NerdWallet’s comparison tables to really see those tier breakdowns.

I personally think the easiest programs to manage are those structured around simple purchase rebates. For example, Fidelity Cash Management Account, while not strictly a “rewards” checking, gives you unlimited ATM fee reimbursements globally, which is a huge win if you travel abroad at all—no more worrying about those $5 or $7 foreign withdrawal fees. That’s tangible value replacing bureaucratic hurdles.

But the absolute worst are the ones that make you opt-in to categories quarterly. You get an email saying, “Hey, this quarter, choose between Gas Stations, Streaming Services, or Restaurants!” Fine, I’ll pick Gas. Then you forget in Month Two, only to realize you made a massive purchase in the Streaming Services category you abandoned, and you missed out on the extra 3% back. That constant vigilance is exhausting, and honestly, that’s why so many people just stick with basic Chase or Bank of America accounts—zero effort, zero rewards. You can read more about the structure of different bank tiers over at Investopedia.

For true cash back specifically, I’ve seen programs where you get 1% back on everything, but you have to maintain a minimum daily balance of around $1,500 just to keep the card functional for earning. If you dip below that for even one day because you paid a big bill, you get zero rewards for the entire statement cycle. It’s a delicate dance, and one missed step costs you. A similar model often requires you to enroll in some kind of online banking portal, which frankly, I find totally unnecessary for spending money. Federal guidance on these structured accounts is often discussed by the CFPB if you want a neutral overview of consumer protection.

If you’re looking primarily at maximizing the pure interest rate and don’t mind linking accounts at different institutions, look at providers that partner with fintech services; sometimes they offer temporary sign-up bonuses, maybe $200 if you deposit $2,000 within 60 days. It’s practically free money if you’re already moving funds around.

It’s amazing how many hidden fees they can slap onto an account that theoretically pays you to use it.